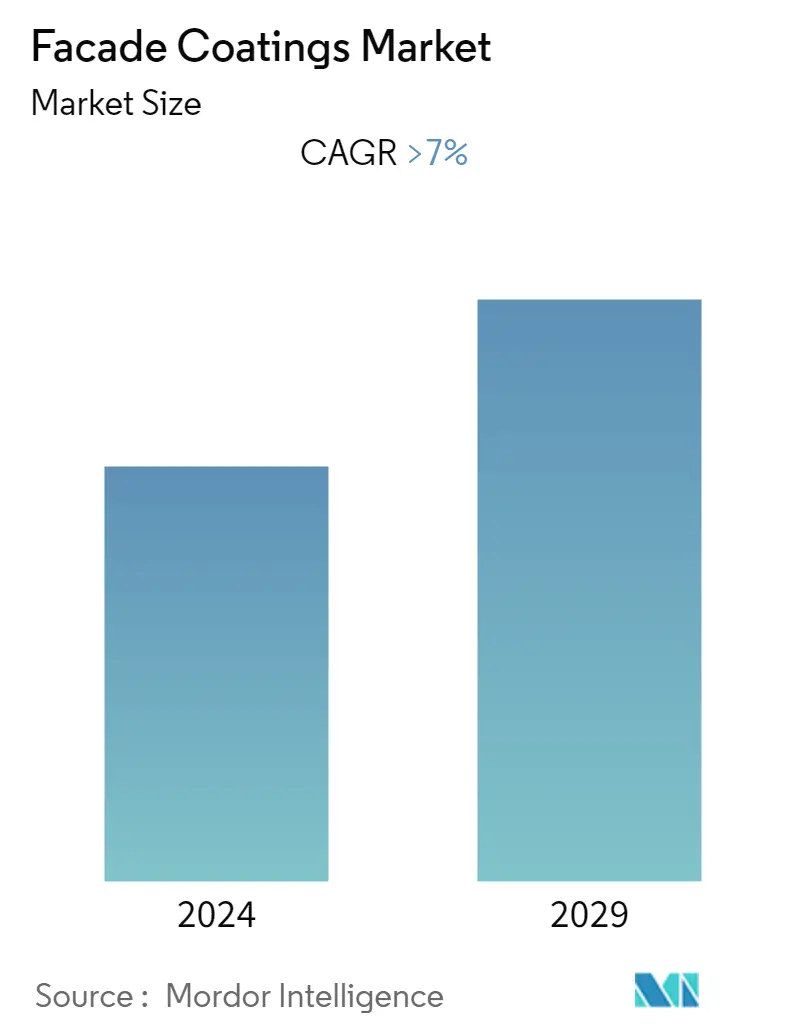

Facade Coatings Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | > 7.00 % |

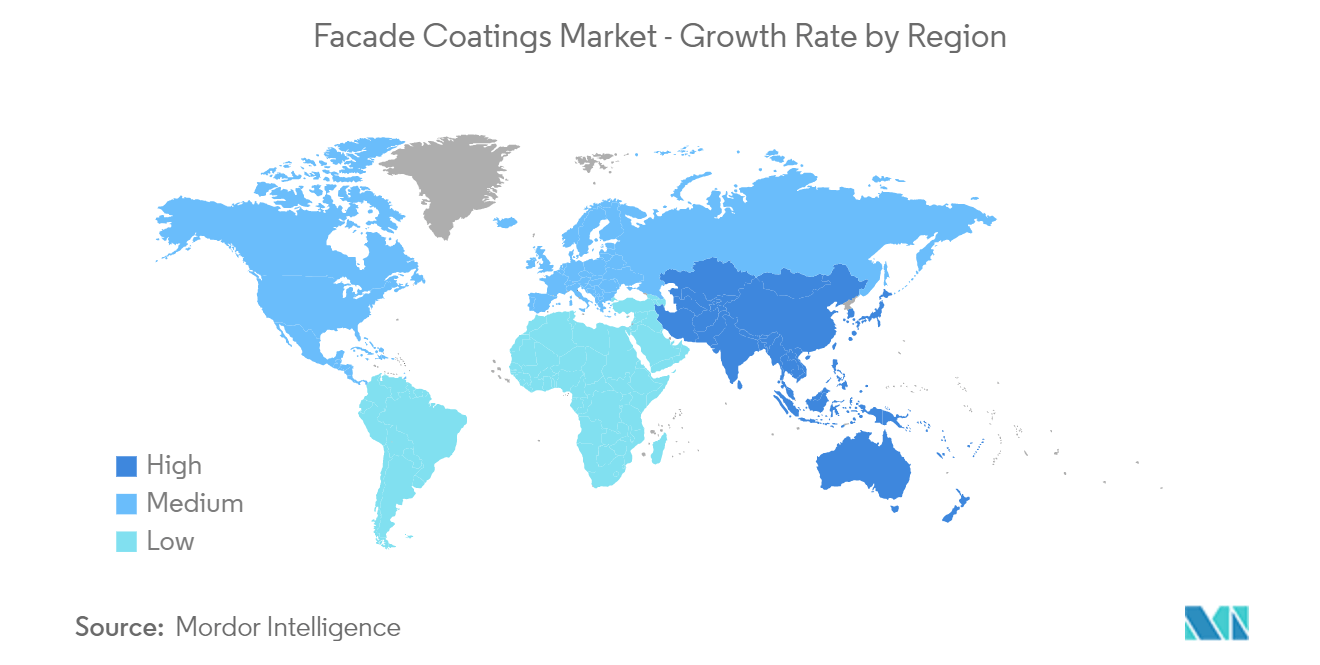

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

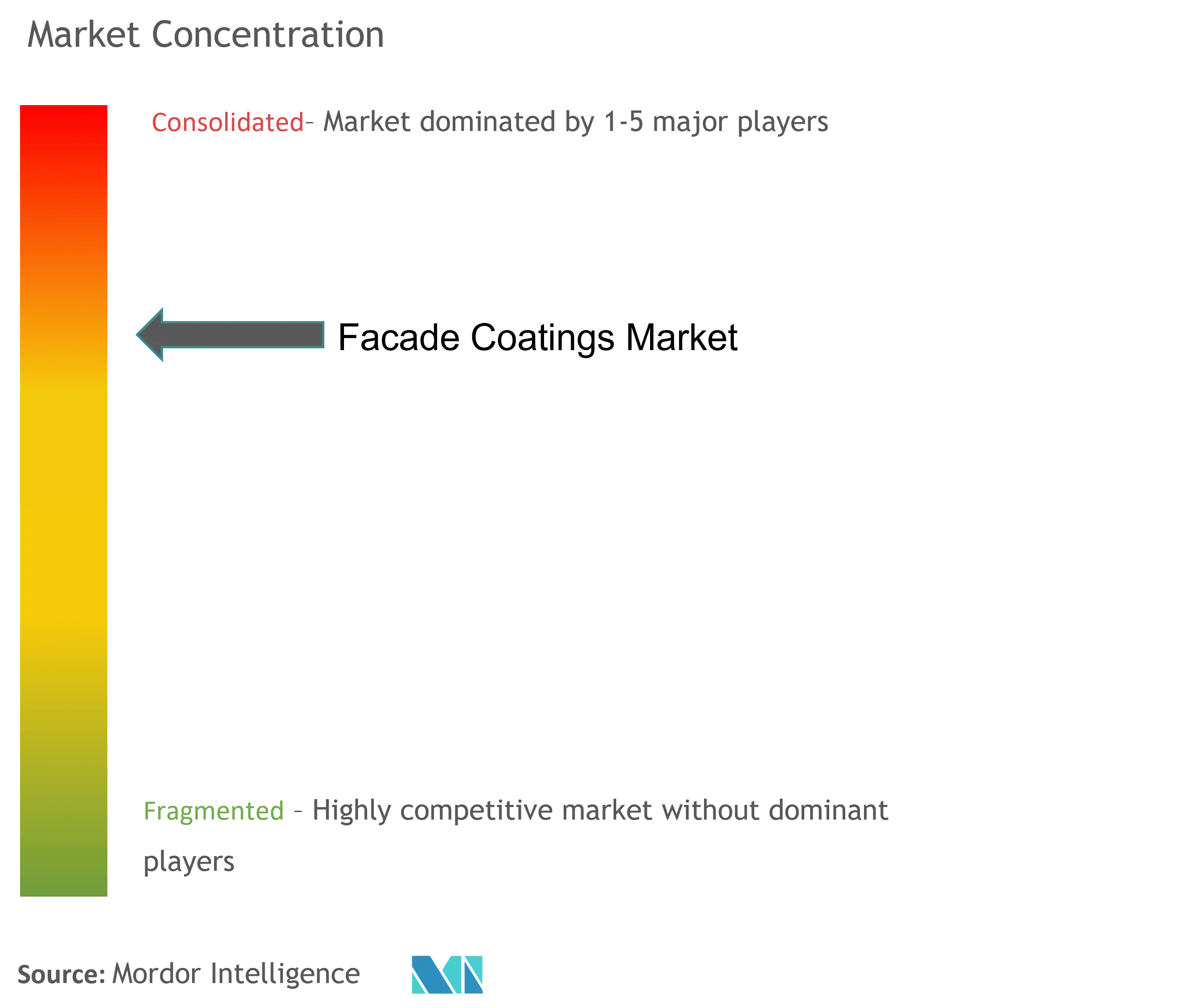

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Facade Coatings Market Analysis

The market for facade coatings is expected to register a CAGR of more than 7% during the forecast period.

The COVID-19 pandemic severely impacted the construction industry due to the temporary lockdowns and disruptions in manufacturing activities, thus negatively affecting the market. However, since 2021, conditions began improving, resuming the market's growth trajectory for the projection period.

- The major factors driving the market studied are the increasing demand from growing residential construction activities and the growing demand for repair in the construction sector.

- On the contrary, the corrosion problems and the leakage issues faced after the coatings will likely hinder the market growth.

- Nevertheless, technological innovations that would lead to the development of energy-saving facade materials may act as an opportunity for the market's future.

- The Asia-Pacific region dominated the global market with the largest consumption in countries such as India, China, and others.

Facade Coatings Market Trends

Residential Segment to Witness Strong Growth

The growing middle-class population, combined with rising disposable income, aided in expanding the middle-class housing segment, increasing the use of facade coatings during the forecast period.

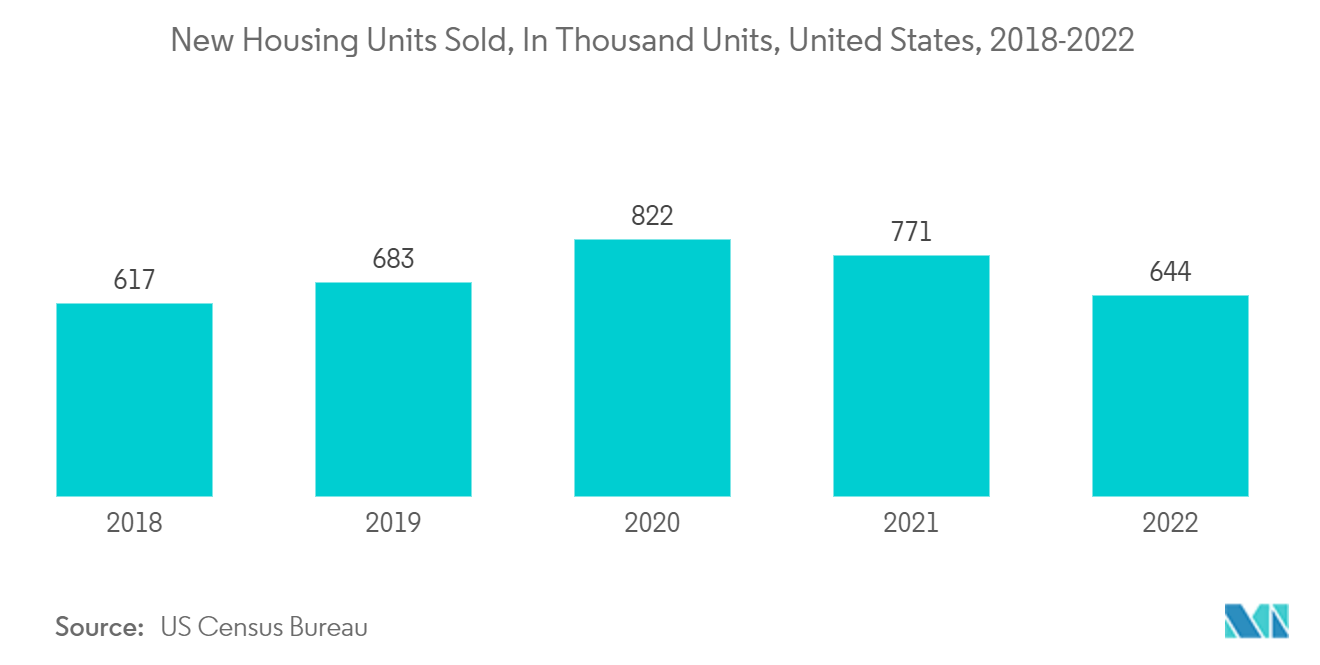

According to the United States Census Bureau, the yearly value of new construction in the United States in 2022 was USD 1,792,854 million, up from USD 1,626,444 million in 2021. Furthermore, the annual value of residential construction in the United States was evaluated at USD 908 billion in 2022, a 13% rise from USD 803 billion in 2021.

Also, according to the US Census Bureau, the seasonally adjusted annual rate of privately owned dwelling units approved by building permits in January 2023 was 1,339,000, a 0.1 percentage point higher than the revised December estimate of 1,337,000. According to the same US Census Bureau statistics release, privately owned housing completions in January 2023 were at a seasonally adjusted annual rate of 1,406,000, up 1.0 percent from the revised December estimate of 1,392,000 and 12.8 percent from the January 2022 pace of 1,247,000.

Aside from new home development, the United States invests heavily in home improvements. The necessity for rehabilitation has become increasingly critical as the country's migrant population has grown. In addition, the increased awareness of the importance of sustainability and high-efficiency constructions has fueled the restoration trend.

Eurostat, in its report, also stated that construction in housing accounted for about 5.6% of the European Union GDP in 2021. This proportion varied across the EU, ranging from 7.6% in Cyprus to 7.2% in Germany and Finland, 1.3% in Greece, 2.1% in Ireland, 2.2% in Latvia, and 2.3% in Poland.

According to the Ministry of Housing, Communities, and Local Government (United Kingdom), 177,820 dwellings were completed in 2022 in England, compared to 174,930 dwellings completed in 2021. Furthermore, according to a recent House of Commons report published in 2022, the number of households in England is expected to increase gradually to 26.9 million units by 2043, representing an annual increase of approximately 150,000 households.

Germany also approved the construction of 25,399 dwellings for October 2022. According to the Federal Statistics Office (Destatis), this reflects a 14.2% decrease in building permits from October 2021. Also, 297,453 residential building licenses were issued between January and October 2022.

All the above factors will likely increase the demand for the facade coatings market over the forecast period.

Asia-Pacific Region to Dominate

Owing to the highest residential construction activity and commercials in the Asia-Pacific region, the facade construction and its coatings accounted for the highest market share among other regional markets.

Across the Asia-Pacific region, demand for residential construction has risen due to the growing population and rapid urbanization across major economies. As per a joint study conducted by Global Construction Perspectives and Oxford Economics, India will require to build 31,000 homes every day for the next 14 years to meet the growing housing demand in the country, adding up to a total of 170 million properties by the end of 2030.

According to the Ministry of Statistics and Program Implementation, the construction sector contributed INR 2,590.98 billion (~USD 31.52 billion) to GDP in the third quarter of 2022. Furthermore, the Indian government allocated INR 48,000 crores (~USD 6.4 billion) for its 'PM Aawas Yojana' scheme in its Union Budget 2022-23, reiterating its commitment to implementing 'Housing for All,' which aims to build 80,00,000 affordable homes for the urban and rural poor in FY 2022-23. The government subsequently extended the timeline for the 'PM Aawas Yojana' scheme for rural areas in December 2022 and amended the objective to 2.95 crores (~29.5 million) dwellings.

China's construction industry is rapidly increasing and is the largest in Asia-Pacific. According to the National Bureau of Statistics of China, construction output in China in the fourth quarter of 2022 was valued at roughly CNY 276 billion (~USD 40 billion), marking a 50% increase over the previous quarter (~USD 27.6 billion).

Indonesia is also one of the largest and fastest-growing marketplaces in Southeast Asia. Furthermore, the Indonesian government has begun a program to develop approximately one million housing units throughout Indonesia, for which the government has budgeted approximately USD 1 billion.

According to Japan's Ministry of Land, Infrastructure, Transport, and Tourism (MLIT), overall investment in the construction sector in 2022 is expected to be around JPY 66,990 billion (~USD 508.16 billion), a 0.6% increase over the previous year.

All the factors above will likely increase the demand for facade coatings in the Asia-Pacific region over the forecast period.

Facade Coatings Industry Overview

The Facade Coatings Market is partially consolidated. A few major players account for the majority of the market share. The top players in the market include (not in any particular order) A&I Coatings, PPG Industries Inc., The Sherwin-Williams Company, Axalta Coating Systems, and Sika AG, amongst others.

Facade Coatings Market Leaders

A&I Coatings

Axalta Coating Systems

PPG Industries Inc

The Sherwin-Williams Company

Sika AG

*Disclaimer: Major Players sorted in no particular order

Facade Coatings Market News

- Recent developments pertaining to the market studied will be covered in the complete report.

Facade Coatings Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand From Growing Residential Construction Activities

4.1.2 Growing Demand From Repairment in Construction sector

4.2 Restraints

4.2.1 Corrosion Problems and Leakage Issues Faced After Coating

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Regulatory Policies

5. MARKET SEGMENTATION (Market Size in Value)

5.1 Resin Type

5.1.1 Silicone

5.1.2 Epoxy

5.1.3 Acrylic

5.1.4 Polyurethane

5.1.5 Others

5.2 End-User

5.2.1 Residential

5.2.2 Industrial

5.2.3 Commercial

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share(%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 A&I Coatings

6.4.2 AkzoNobel NV

6.4.3 Axalta Coating Systems

6.4.4 Brillux GmbH & Co. KG

6.4.5 DAW SE

6.4.6 Nippon Paint Company Limited.

6.4.7 PermaRock

6.4.8 PPG Industries, Inc.

6.4.9 ProPerla

6.4.10 Remmers Limited

6.4.11 RPM International Inc.

6.4.12 San Marco Group S.p.A.

6.4.13 The Sherwin-Williams Company

6.4.14 Sika AG

6.4.15 Specialized Coating Systems (Pty) Ltd

6.4.16 Sto SE & Co. KGaA

6.4.17 Teknos Group

6.4.18 Tikkurila

6.4.19 Wacker Chemie AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Technological Innovations Leading to Development of Energy-Saving Facade Materials

Facade Coatings Industry Segmentation

A facade is generally the front part of a building of any type that is visible to people from the outside. Facade coatings are the type of coatings that are done on the outside of the walls in order to protect the structure of the walls along with providing an aesthetic design.

The Facade Coatings Market is segmented by resin type, end-user, and Geography. By resin type, the market is segmented into silicone, epoxy, acrylic, polyurethane, and other types. By end-user, the market is segmented into residential, industrial, and commercial. The report also covers the market size and forecasts for the facade coatings market in 15 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD million).

| Resin Type | |

| Silicone | |

| Epoxy | |

| Acrylic | |

| Polyurethane | |

| Others |

| End-User | |

| Residential | |

| Industrial | |

| Commercial |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Facade Coatings Market Research FAQs

What is the current Facade Coatings Market size?

The Facade Coatings Market is projected to register a CAGR of greater than 7% during the forecast period (2024-2029)

Who are the key players in Facade Coatings Market?

A&I Coatings, Axalta Coating Systems, PPG Industries Inc, The Sherwin-Williams Company and Sika AG are the major companies operating in the Facade Coatings Market.

Which is the fastest growing region in Facade Coatings Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Facade Coatings Market?

In 2024, the Asia Pacific accounts for the largest market share in Facade Coatings Market.

What years does this Facade Coatings Market cover?

The report covers the Facade Coatings Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Facade Coatings Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Facade Coatings Industry Report

Statistics for the 2024 Facade Coatings market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Facade Coatings analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.