Automotive Semiconductor Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR (2024 - 2029) | 14.43 % |

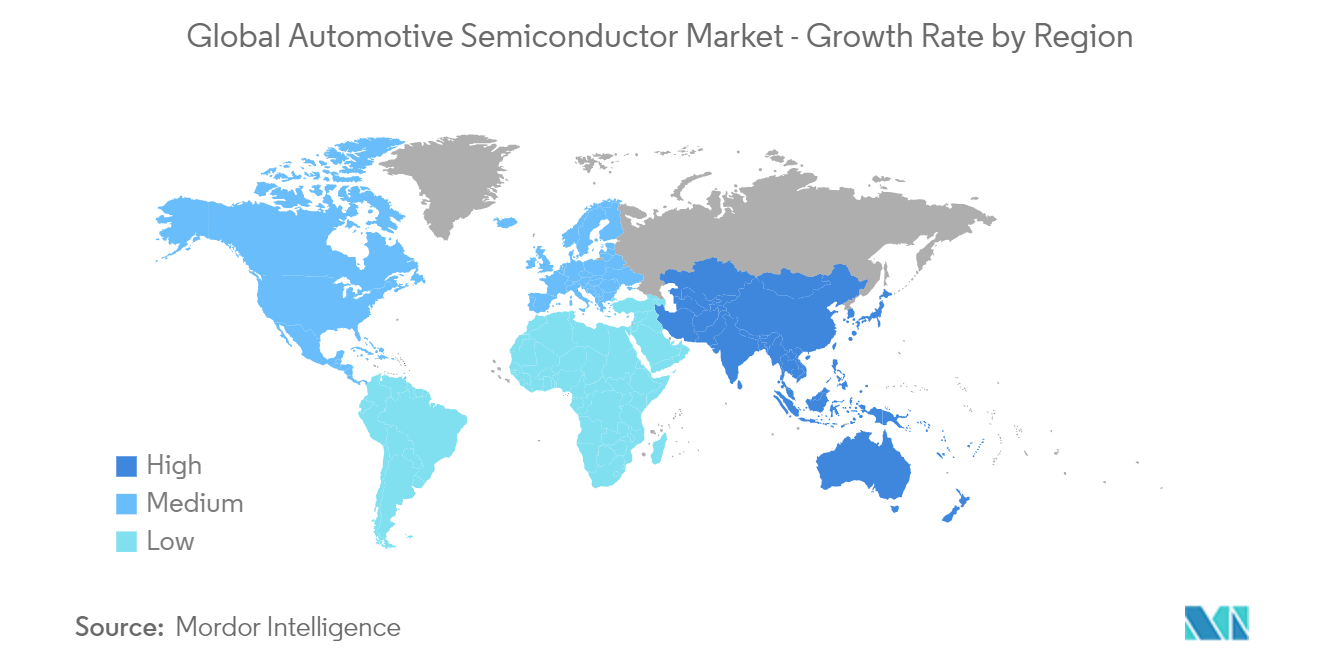

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

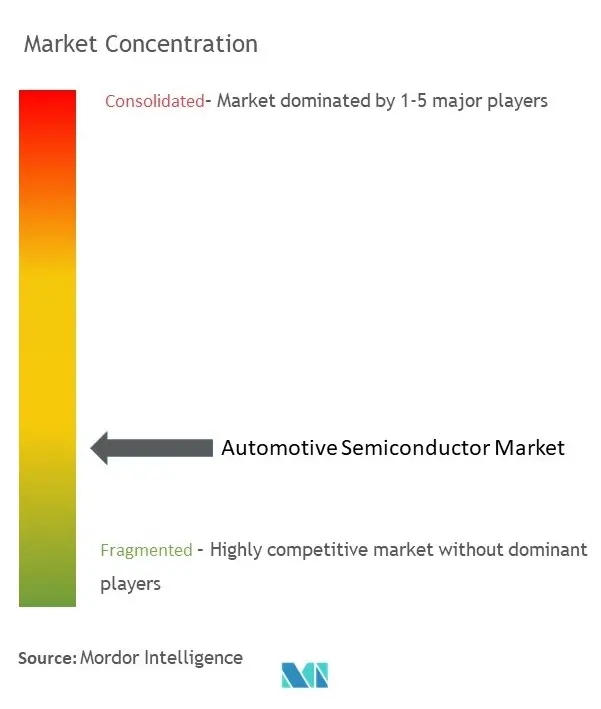

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Automotive Semiconductor Market Analysis

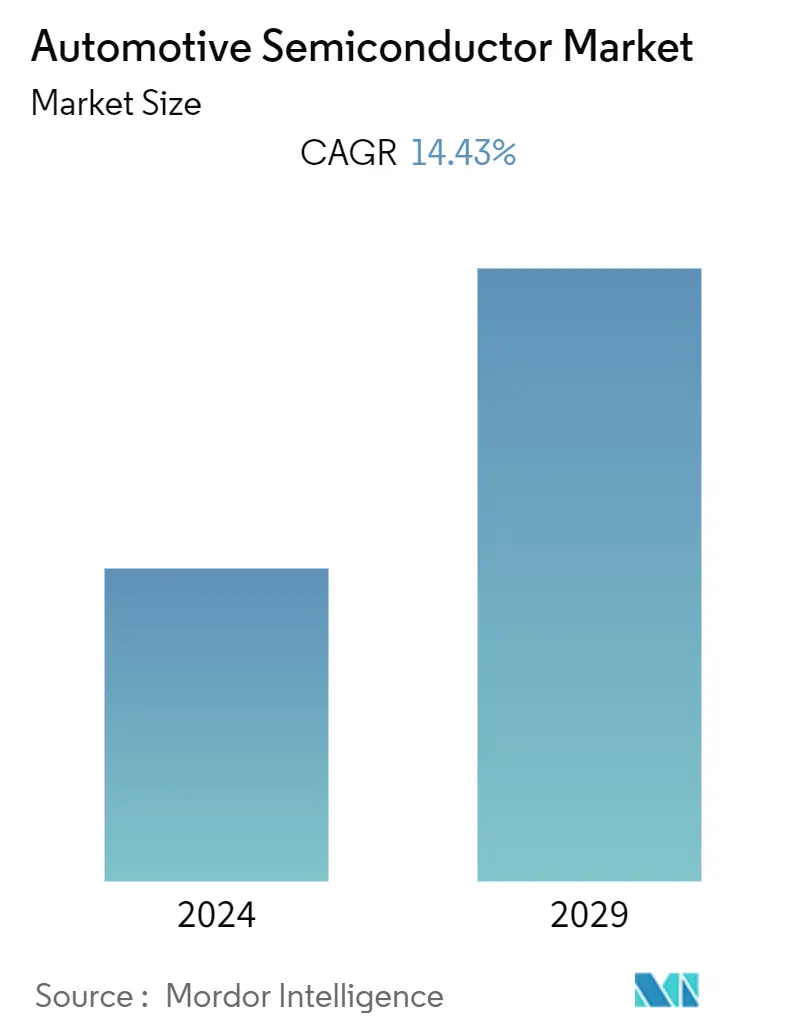

The Automotive Semiconductor Market is expected to register a CAGR of 14.43% during the forecast period.

The automotive semiconductor market size is expected to grow from USD 71.62 billion in 2023 to USD 140.52 billion by 2028, at a CAGR of 14.43 percent during the forecast period (2023-2028). The market was evaluated by analyzing the sizes of components used in the automotive industry, including processors, sensors, memory devices, integrated circuits, and discrete power devices. The report's scope comprises analyzing various vehicle types, like light commercial vehicles, heavy commercial vehicles, and passenger vehicles, around the world.

- A semiconductor is a substance, such as germanium or silicon, with electrical conductivity intermediate between a conductor and an insulator. The application of semiconductors in vehicles ranges from chassis, power electronics safety, body electronics, and comfort or entertainment units.

- Automobiles are an essential element of people's lives because they are the primary form of transportation today. The automotive safety and security system technologies have undergone a significant change in recent years, from seat headrests to adaptive cruise control systems. The rising wave of advanced technologies, such as blind-spot detection, drowsiness monitoring systems, lane departure warning systems, head-up display, night vision systems, park assist, e-call telematics, and tire-pressure-monitoring system technologies, are creating a significant potential for safety and security systems to protect the driver and passengers from severe injuries during a vehicle crash. The increasing adoption of autonomous vehicles is expected to drive the growth of the studied market. For instance, according to Intel, global car sales are estimated to reach more than 101.4 million units in 2030, and autonomous vehicles are anticipated to account for approximately 12 percent of car registrations by 2030.

- A growing number of affordable vehicles feature advanced infotainment, safety, performance, and fuel efficiency. Such features lead to the inclusion of various components, leading to an increase in the price raise of the overall vehicle. Thousands of semiconductor chips are at the core of automobiles today, acting as the vehicle's eyes, ears, and brain, monitoring the environment, making choices, and regulating actions. According to the Semiconductor Industry Association, modern automobiles may have 8,000 or more semiconductor chips and over 100 electronic control units, which account for more than 35 percent of total vehicle cost and are predicted to exceed 50 percent by 2025 to 2030.

- The increase in automotive production is also estimated to offer lucrative opportunities for the studied market. For instance, according to OICA, in 2022, around 85 million automobiles will be produced worldwide. It represents an increase of around 6 percent over the previous year. Further, according to the China Association of Automobile Manufacturers(CAAM), in January 2022, approximately 345,000 commercial vehicles and 2.08 million passenger cars were manufactured in China. The industry, in total, produced 2.42 million vehicles in January 2022.

- Moreover, according to the Society of Motor Manufacturers and Traders, British commercial vehicle production grew by 39.3 percent (as compared to 2021) to 101,600 units in 2022. The output for the domestic market in 2022 rose by 14.0 percent year-on-year to 40,409 units, with 101,600 vans, trucks, taxis, buses, and coaches leaving factory lines. The increased automotive manufacturing activities would aid the growth of the studied market during the forecast period.

- COVID-19 caused an immediate halt in existing manufacturing, impacting supply chains worldwide. China, which was initially afflicted by the pandemic, lost over two-thirds of its vehicle manufacturing due to the statewide lockdown, significantly damaging the supply chain. Auto supply chains are frequently geographically dispersed; with each country imposing its protocol following the pandemic, supply chain management took a significant hit, emerging as one of the most critical challenges confronting the automotive industry during COVID-19.

- The high costs associated with developing and deploying automotive semiconductors are anticipated to significantly restrain the studied market.

Automotive Semiconductor Market Trends

Heavy Commercial Vehicle Segment to Register Significant Growth

- The heavy commercial vehicle market is expected to register a significant CAGR during the projected period. With the introduction of modern technology, such as accident prevention systems, ADAS, efficient driving and engine systems, and a focus on environmental sustainability and emission reduction, the demand for these large commercial vehicles will likely increase.

- Top manufacturers' technological advancements in heavy commercial vehicles are set to surge worldwide. A prominent trend characterizing the market's success has concentrated on accident prevention systems, automatic emergency braking systems, driver assistance, and blind-spot monitoring. Installing automated emergency braking systems and forward-collision warnings on heavy-duty vehicles may save more than 40 percent of rear-end incidents involving large trucks, according to research led by the Insurance Institute for Highway Safety (IIHS).

- According to the research, heavy-duty vehicles with front-crash prevention systems, such as automated emergency braking (AEB), had 12 percent fewer collisions, and forward-collision warning (FCW) had 22 percent fewer collisions, compared to vehicles without front-crash prevention systems. Consequently, the increasing demand for integrated ICs to make efficient automatic braking and driving systems significantly drives the automotive semiconductor market worldwide.

- Under the new scrappage policy, governments in Asia-Pacific countries, like India, South Korea, and China, seek to push heavy-duty truck owners to acquire new heavy-duty trucks and other commercial vehicles, discouraging the use of old, polluting ones. The program would reduce pollution levels and promote the advancements of the heavy trucks segment in adopting integrated ICs, sensors, advanced microcontrollers, ADAS, and motor driver ICs, significantly influencing the market's growth.

- Several heavy-duty truck manufacturers in Europe have been investing in integrating novel technology to meet the zero-emission objective from 2025 onwards to avoid paying high penalties for non-compliance with EU norms. The European Union has established carbon-neutrality goals and criteria for heavy-duty vehicles. These include a 15 percent decrease beginning in 2025 and increasing to 30 percent by 2030, with zero emissions by 2050.

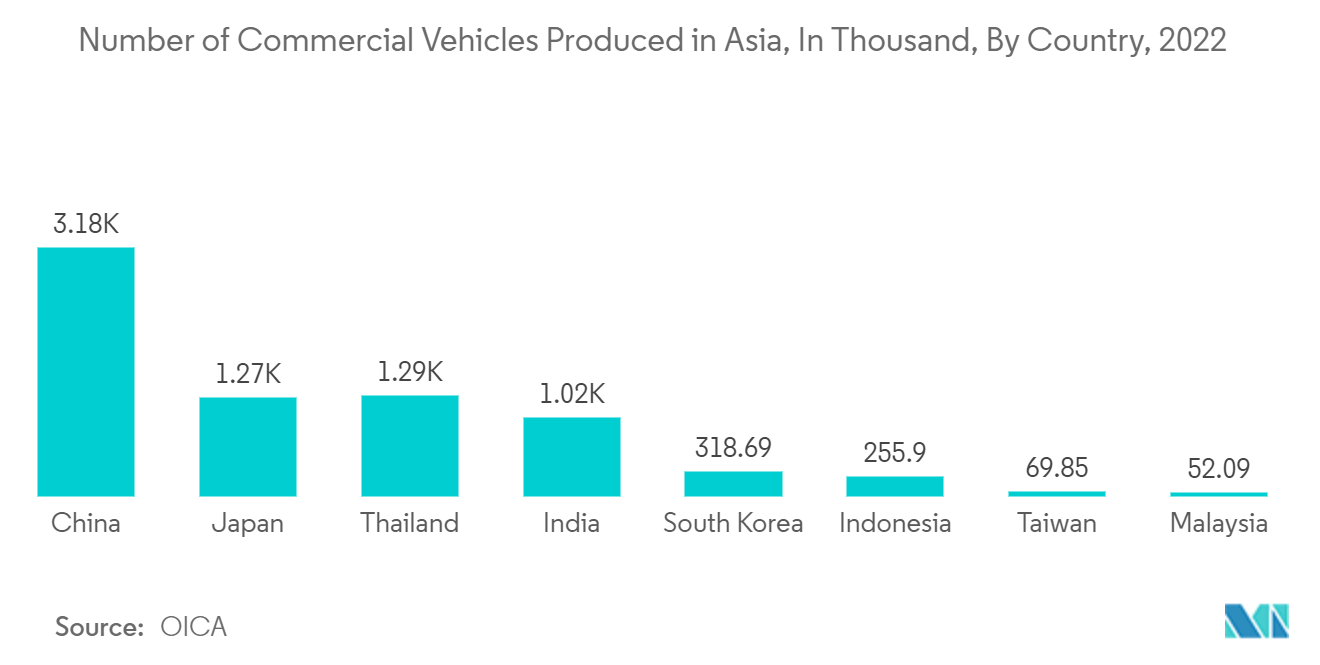

- According to OICA, in 2022, China produced the highest number of commercial vehicles in the Asia-Pacific region, with around 3.18 million units. In the same year, Japan produced approximately 1.27 million commercial vehicles.

Asia-Pacific to be the Fastest Growing Region

- The Asia-Pacific automotive semiconductor market is fueled by increased automotive manufacturing and continued partnerships between automotive OEMs and semiconductor manufacturers. Cost and fuel efficiency are no longer the most important factors to consider when buying an automobile; instead, the comfort and luxury offered by the vehicle are more important.

- This may be attributed to the fact that global automobile manufacturers are seeing strong demand for luxury and semi-luxury vehicles, which is pressuring them to install more electronic components, pushing the Asia-Pacific automotive semiconductors market. As a result of this reason, the Asia-Pacific automotive semiconductor industry offers a potential market area.

- The rapid expansion of the Asia-Pacific automotive semiconductor industry is expected to be fueled by the rising demand for electric vehicles. Automobile manufacturers must continue to innovate, create, and develop self-driving cars, which have already attracted a significant number of customers in key automotive manufacturing countries.

- The growth trajectory of fully autonomous automobiles is expected to be heavily influenced by several factors, including technology advancements, consumer willingness to accept fully automated vehicles, pricing, and suppliers' and OEMs' capacity to address major concerns about vehicle safety.

- According to the automobile industry, two-wheelers, three-wheelers, and tractors are in great demand across the country. In addition, India has a strong semiconductor R&D infrastructure, which may open up new potentials for the automotive semiconductor market in India in the future. Further, the government is taking various initiatives to boost the supply of semiconductor chips in the country. For instance, in September 2022, the Indian government announced to provide uniform fiscal support of 50 percent of the project cost for setting up semiconductor fabrication plants to boost semiconductor manufacturing in the country.

Automotive Semiconductor Industry Overview

The automotive semiconductor market is highly fragmented due to the presence of major players like NXP Semiconductor NV, Infineon Technologies AG, Renesas Electronics Corporation, STMicroelectronics NV, and Toshiba Electronic Devices& Storage Corporation (Toshiba Corporation), among others. Players in the market are adopting strategies such as partnerships, mergers, collaborations, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In July 2023, Renesas Electronics Corporation announced a development board for automotive gateway systems. The R-Car S4 Starter Kit is a low-cost, readily available development board for building software using the Renesas R-Car S4 system on a chip. (SoC).

In June 2023, Intellias announced its partnership with Elmos Semiconductor to reinforce Elmos with software engineering expertise and support development processes to create software for lighting, ranging, and optical sensors used in the most modern vehicles.

In August 2022, Onsemi opened a silicon carbide (SiC) facility in Hudson, New Hampshire. The facility is expected to increase the company's production capacity by five times yearly and almost quadruple the number of employees in Hudson by the end of 2022.

In July 2022, NXP Semiconductors NV collaborated with Foxconn for a new generation of intelligent connected vehicles. The primary focus of the collaboration is aimed at Foxconn's efforts in electric vehicle platforms, leveraging the company's system expertise and comprehensive portfolio. The collaboration would leverage NXP's portfolio of automotive technologies and its expertise in safety and security to enable architectural innovation and platforms for electrification, connectivity, and safe automated driving.

Automotive Semiconductor Market Leaders

NXP Semiconductor NV

Infineon Technologies AG

Renesas Electronics Corporation

STMicroelectronics NV

Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation)

*Disclaimer: Major Players sorted in no particular order

Automotive Semiconductor Market News

- June 2023 - Nidec Corporation and Renesas Electronics Corporation announced a collaboration to develop semiconductor solutions for a next-generation E-Axle (X-in-1 system) that integrates an EV drive motor and power electronics for electric vehicles (EVs).

- June 2023 - SK Hynix Inc. announced that the company had received the automotive ASPICE Level 2 certification for automotive memory solution development. The accreditation, essential for automotive NAND solution products, is expected to increase the supply and stronger profitability of the company's NAND solution products, such as Universal Flash Memory and Solid State drive.

- October 2022: Micron Technology Inc. intended to invest up to USD 100 billion over the coming 20-plus years to construct a new mega fab in Clay, New York, with the first phase investment of USD 20 billion planned by the end of the following decade. Micron's New York mega fab is part of its strategy to gradually increase American-made leading-edge DRAM production to 40 percent of its global output over the next decade. Micron's DRAM production in the United States benefits its customers tremendously, enabling them to build innovative products.

- June 2022: NXP Semiconductors NV announced new processor families that extend the benefits of the company's innovative S32 automotive platform with high-performance real-time processing and safety. The S32E and S32Z processor families help the automotive industry boost the integration of diverse real-time applications for domain and zonal control, vehicle electrification, and safety processing that are critical for safer and more efficient vehicles.

- June 2022: Renesas Electronics Corporation developed circuit technologies for 22 nm embedded STT-MRAM with faster read and write execution for microcontrollers in IoT applications. The test chip includes a 32-megabit embedded MRAM memory cell array and executes 5.9 nanosecond random read credentials at a maximum junction temperature of 150°C and a write throughput of 5.8-megabyte-per-second.

Automotive Semiconductor Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Intensity of Competitive Rivalry

4.2.5 Threat of Substitute Products

4.3 Industry Value Chain Analysis

4.4 Assessment of the Impact of Key Macroeconomic Trends on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Vehicle Production

5.1.2 Rising Demand for Advanced Safety and Comfort Systems

5.2 Market Restraints

5.2.1 Higher Cost of Advanced Featured Vehicles

6. MARKET SEGMENTATION

6.1 By Vehicle Type

6.1.1 Passenger Vehicle

6.1.2 Light Commercial Vehicle

6.1.3 Heavy Commercial Vehicle

6.2 By Component

6.2.1 Processors

6.2.2 Sensors

6.2.3 Memory Devices

6.2.4 Integrated Circuits

6.2.5 Discrete Power Devices

6.3 By Application

6.3.1 Chassis

6.3.2 Power Electronics

6.3.3 Safety

6.3.4 Body Electronics

6.3.5 Comforts/Entertainment Unit

6.3.6 Other Applications

6.4 By Geography

6.4.1 North America

6.4.2 Europe

6.4.3 Asia-Pacific

6.4.4 Latin America

6.4.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 NXP Semiconductor NV

7.1.2 Infineon Technologies AG

7.1.3 Renesas Electronics Corporaton

7.1.4 STMicroelectronics NV

7.1.5 Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation)

7.1.6 Texas Instrument Inc.

7.1.7 Robert Bosch GmbH

7.1.8 Micron Technology

7.1.9 Onsemi (Semiconductor Components Industries LLC)

7.1.10 Analog Devices Inc.

7.1.11 ROHM Co. Ltd

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE TRENDS

Automotive Semiconductor Industry Segmentation

Semiconductors are materials that have a conductivity between conductors (generally metals) and non-conductors or insulators (such as ceramics). Modern cars contain features like cell phone integration, heads-up displays, autonomous driving aids, comfort, and performance. As cars become even more complicated, demand for automotive semiconductors is expected to increase steadily and provide a powerful long-term growth engine for the automotive industry.

Global automotive semiconductor industry report covers top automotive semiconductor companies and is segmented by vehicle type (passenger vehicle, light commercial vehicle, and heavy commercial vehicle), by component (processors, sensors, memory devices, integrated circuits, and discrete power devices), by application (chassis, power electronics, safety, body electronics, comfort/entertainment unit, and other applications), and by geography (North America, Europe, Latina America, Asia-Pacific, and Middle East and America). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Vehicle Type | |

| Passenger Vehicle | |

| Light Commercial Vehicle | |

| Heavy Commercial Vehicle |

| By Component | |

| Processors | |

| Sensors | |

| Memory Devices | |

| Integrated Circuits | |

| Discrete Power Devices |

| By Application | |

| Chassis | |

| Power Electronics | |

| Safety | |

| Body Electronics | |

| Comforts/Entertainment Unit | |

| Other Applications |

| By Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East and Africa |

Automotive Semiconductor Market Research FAQs

What is the current Automotive Semiconductor Market size?

The Automotive Semiconductor Market is projected to register a CAGR of 14.43% during the forecast period (2024-2029)

Who are the key players in Automotive Semiconductor Market?

NXP Semiconductor NV, Infineon Technologies AG, Renesas Electronics Corporation, STMicroelectronics NV and Toshiba Electronic Devices & Storage Corporation (Toshiba Corporation) are the major companies operating in the Automotive Semiconductor Market.

Which is the fastest growing region in Automotive Semiconductor Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Automotive Semiconductor Market?

In 2024, the North America accounts for the largest market share in Automotive Semiconductor Market.

What years does this Automotive Semiconductor Market cover?

The report covers the Automotive Semiconductor Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Automotive Semiconductor Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the factors driving the Automotive Semiconductor Market?

The key factors driving the Automotive Semiconductor Market are a) Increasing demand for advanced driver-assistance systems (ADAS) b) Growing demand for electric vehicles c) Increasing comfort and safety features in cars

Automotive Semiconductor Industry Report

The global automotive semiconductor market is witnessing significant growth, driven by the increased adoption of electric and hybrid vehicles, the surge in demand for advanced vehicle safety and comfort systems, and the introduction of innovative technologies for an advanced user interface. However, the market faces challenges such as operational failures in extreme climatic conditions and the global chip shortage. Despite these hurdles, the market offers substantial growth opportunities, especially with the rising demand for advanced power semiconductors for improved performance and operational efficiency, and the emergence of autonomous vehicles. The market is segmented into component, vehicle type, propulsion type, and application, with Asia-Pacific dominating due to the integration of IoT and AI in the region's automotive industry. The advent of autonomous vehicles offers a unique opportunity for semiconductor manufacturers to partake in a technological shift. Businesses capable of providing reliable, high-performance, and energy-efficient semiconductor solutions tailored to autonomous driving are expected to significantly shape the future of transportation. Mordor Intelligence™ Industry Reports provide statistics for the Automotive Semiconductor market share, size, and revenue growth rate, including a market forecast outlook and a historical overview. A sample of this industry analysis is available as a PDF download.