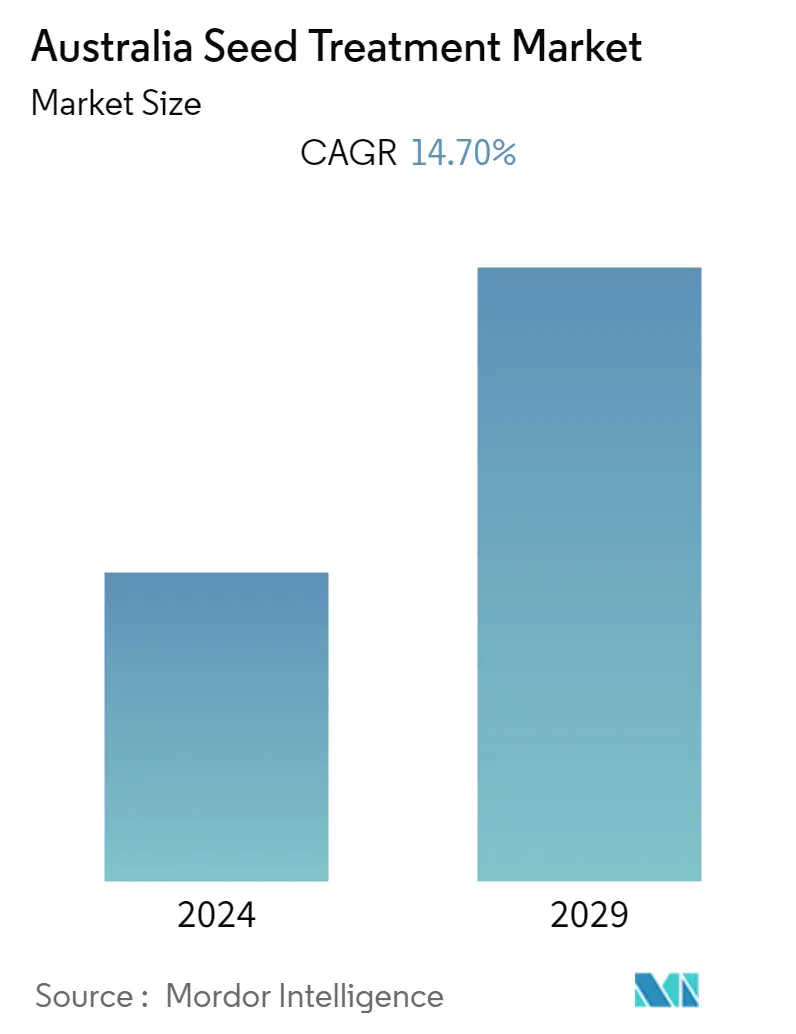

Australia Seed Treatment Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | 14.70 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Australia Seed Treatment Market Analysis

The seed treatment market is projected to register a CAGR of 14.7% during the forecast period (2020-2025). In Australia, chemical seed treatment occupies the highest market share, while the non-chemical seed treatment is the fastest-growing segment in the forecast period. The Australian Pesticides and Veterinary Medicines Authority (APVMA) regulates chemical seed treatments in the country and estimates that the wheat dominates the Australian market with a share of 37%, followed by canola with a share of 26%. The seed treatment market is driven by increasing awareness among the farming community, increasing demand for food grains, and economic growth among countries, among other factors. Various regulations and government agencies are encouraging the use of seed treatments because seed treatment offers effective seed protection from pathogens, insects, and other pests, in addition to contributing to the healthy and uniform stand establishment of a variety of crops produced.

Australia Seed Treatment Market Trends

This section covers the major market trends shaping the Australia Seed Treatment Market according to our research experts:

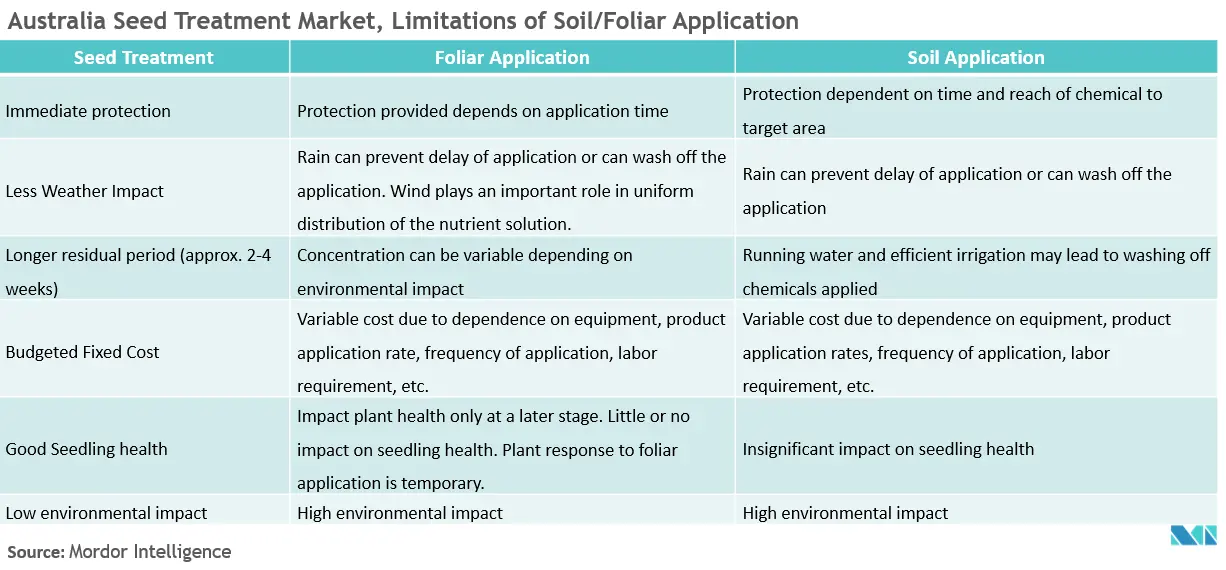

Increasing Limitations Associated With Soil/Foliar Application

Soil and foliar applications of agrochemicals are important tools for the productive management of crops and have significant commercial relevance, globally. Wheat is the leading type of crop for seed treatment applications in Australia. Seed treatment helps with the increased possibility of germination in unfavorable conditions like dry or cold soil, and efficiently sowing in fields with a history of stand establishment problems. As of April 2018, the Australian federal government has proposed compulsory fungicidal treatment for imported seeds of the brassica family, which will lead to an increase in demand for fungicidal seed treatment products in the country. As seed treatments are effective in compacting germination issues and certain seed-borne pathogens and showcasing promising benefits with better sprouting and growth, thereby increasing yield potentials at a minimum additional cost, the seed treatment market is registering a rapid growth.

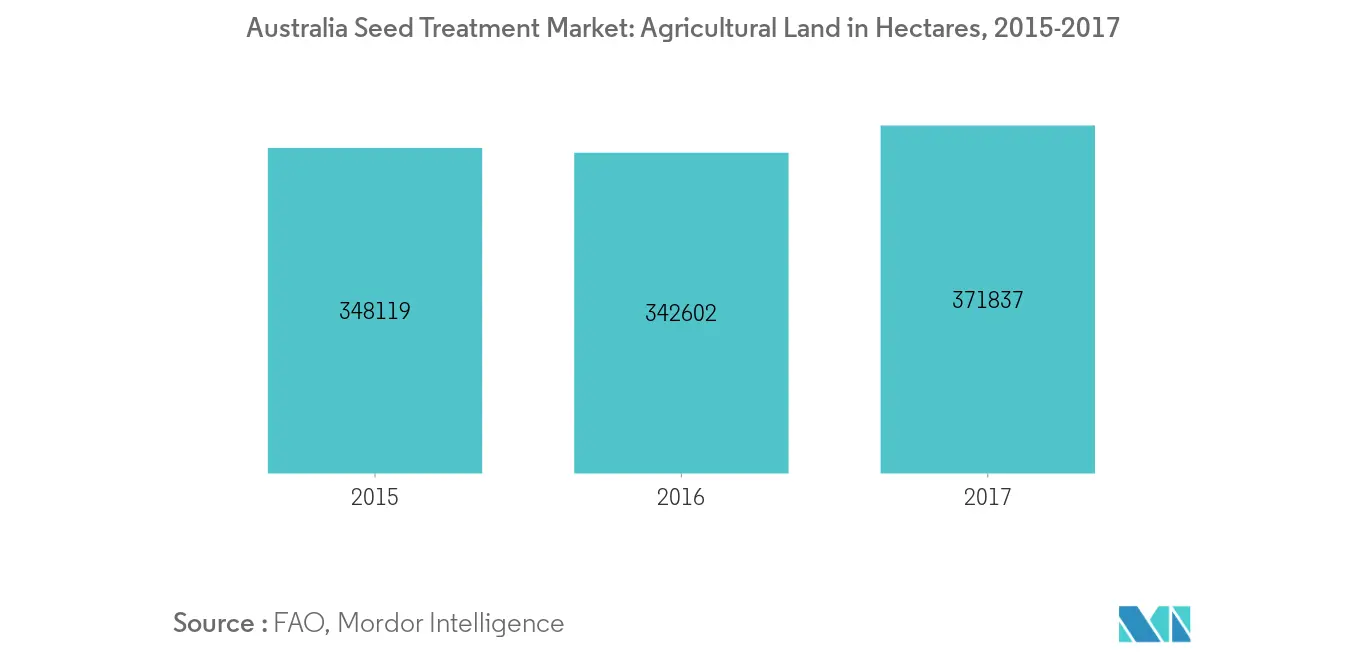

Increase In Farm Sizes

The growing population in the region demands more and more food, though the new area under cultivation has been decreasing at a rapid rate. This, therefore, translates into increasing the sizes of existing farmlands, which gives rise to alterations in management practices. Under such circumstances, farmers tend to undertake early planting in order that their complete acreage is sown. However, the conditions of early sowing may not be optimal, such as the prevalence of cool and wet conditions that are not conducive to planting. This increases the potential of seedling damage, which makes a strong case in favor of risk management techniques. Seed treatment is one such technique that can help in protecting young seedlings against pathogens and insect attacks. The Australian seed treatment market is growing at a rapid rate due to factors such as economic benefits of high yields, better quality, improved returns, better rates of disease control in early sown seeds, protection of high-value seeds, reduced tillage, and cost-effective solution to enhance production, which drives the market.

Australia Seed Treatment Industry Overview

Some of the key companies in the market are Adama, Novozymes, Chemtura, Syngenta, and Others. The key players are focusing to expand their business in Australia. The leading players in this market adopted various strategies to strengthen market opportunities and increase their market shares. Acquisitions, agreements & joint ventures are the major strategies adopted by major players.

Australia Seed Treatment Market Leaders

Adama Agricultural Solutions

BASF SE

Nufarm

Syngenta International AG

Tata Rallis Ltd

*Disclaimer: Major Players sorted in no particular order

Australia Seed Treatment Market Report - Table of Contents

-

1. INTRODUCTION

-

1.1 Study Deliverables

-

1.2 Study Assumptions

-

1.3 Scope of the Study

-

-

2. RESEARCH METHODOLOGY

-

3. EXECUTIVE SUMMARY

-

4. MARKET DYNAMICS

-

4.1 Market Overview

-

4.2 Market Drivers

-

4.3 Market Restraints

-

4.4 Porters Five Force Analysis

-

4.4.1 Threat of New Entrants

-

4.4.2 Bargaining Power of Buyers/Consumers

-

4.4.3 Bargaining Power of Suppliers

-

4.4.4 Threat of Substitute Products

-

4.4.5 Intensity of Competitive Rivalry

-

-

-

5. MARKET SEGMENTATION

-

5.1 Crop Type

-

5.1.1 Grains & Cereals

-

5.1.2 Pulses and Oil seeds

-

5.1.3 Commercial crops

-

5.1.4 Fruits and Vegetables

-

5.1.5 Other Crop Types

-

-

5.2 Product Type

-

5.2.1 Insecticide

-

5.2.2 Fungicide

-

5.2.3 Other Applications

-

-

5.3 Chemical Origin

-

5.3.1 Synthetic

-

5.3.2 Biological

-

-

5.4 Application

-

5.4.1 Commercial

-

5.4.2 Farm Level

-

-

5.5 Application Technique

-

5.5.1 Seed Coating

-

5.5.2 Seed Pelleting

-

5.5.3 Seed Dressing

-

5.5.4 Other Application Techniques

-

-

-

6. COMPETITIVE LANDSCAPE

-

6.1 Most Adopted Strategies

-

6.2 Market Share Analysis

-

6.3 Company Profiles

-

6.3.1 ADAMA Agricultural Solutions Ltd

-

6.3.2 Advanced Biological Marketing Inc.

-

6.3.3 BASF SE

-

6.3.4 Bayer CropScience AG

-

6.3.5 DuPont de Nemours Inc.

-

6.3.6 INCOTEC Group BV

-

6.3.7 Monsanto Company

-

6.3.8 Nufarm Limited

-

6.3.9 Syngenta International AG

-

6.3.10 Sumitomo Chemical Co. Ltd

-

6.3.11 Rallis India Limited

-

6.3.12 FMC Corporation

-

-

-

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

-

8. IMPACT OF COVID-19

Australia Seed Treatment Industry Segmentation

The corporations in seed treatment operate in B2B, as well as B2C business format. Environmental concerns regarding the use of chemical seed treatment agents have been gaining ground, in recent times. Due to this, the market for biological seed treatment agents, that are free of toxic chemicals and provide treatment options on par with or even better than chemical agents, has been in high demand, over the past few years. The Australia Seed Treatment Market is segmented By Chemical Origin (Synthetic and Biological). By Product Type (Insecticides, Fungicides, and Other Product Types), By Application (Commerical and Farm-Level), By Application Technique (Seed Coating, Seed Pelleting, Seed Dressing, and Other Application Techniques), and By Crop Type (Grains and Cereals, Pulses and Oilseeds, Commercial Crops, Fruits and Vegetables, and Other Crop Types)

| Crop Type | |

| Grains & Cereals | |

| Pulses and Oil seeds | |

| Commercial crops | |

| Fruits and Vegetables | |

| Other Crop Types |

| Product Type | |

| Insecticide | |

| Fungicide | |

| Other Applications |

| Chemical Origin | |

| Synthetic | |

| Biological |

| Application | |

| Commercial | |

| Farm Level |

| Application Technique | |

| Seed Coating | |

| Seed Pelleting | |

| Seed Dressing | |

| Other Application Techniques |

Australia Seed Treatment Market Research FAQs

What is the current Australia Seed Treatment Market size?

The Australia Seed Treatment Market is projected to register a CAGR of 14.70% during the forecast period (2024-2029)

Who are the key players in Australia Seed Treatment Market?

Adama Agricultural Solutions, BASF SE, Nufarm, Syngenta International AG and Tata Rallis Ltd are the major companies operating in the Australia Seed Treatment Market.

What years does this Australia Seed Treatment Market cover?

The report covers the Australia Seed Treatment Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Australia Seed Treatment Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Seed Treatment in Australia Industry Report

Statistics for the 2024 Seed Treatment in Australia market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Seed Treatment in Australia analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.