Managed Security Services (MSSP) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

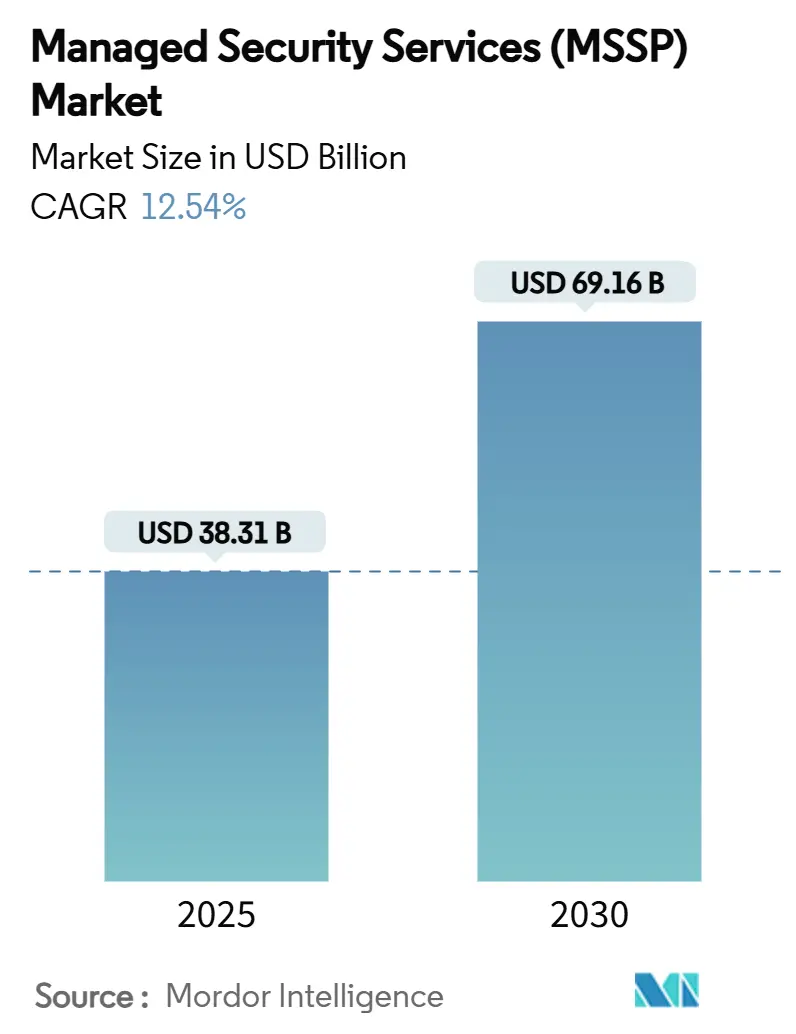

| Market Size (2025) | USD 38.31 Billion |

| Market Size (2030) | USD 69.16 Billion |

| Growth Rate (2025 - 2030) | 12.54% CAGR |

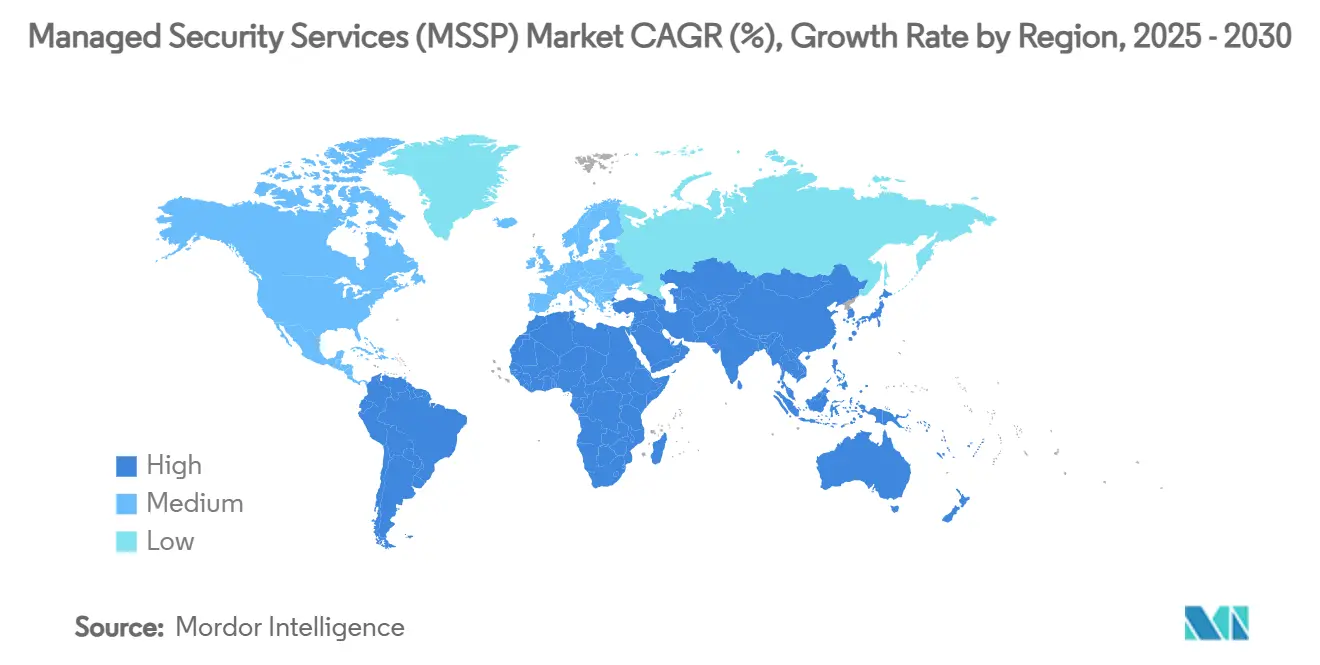

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

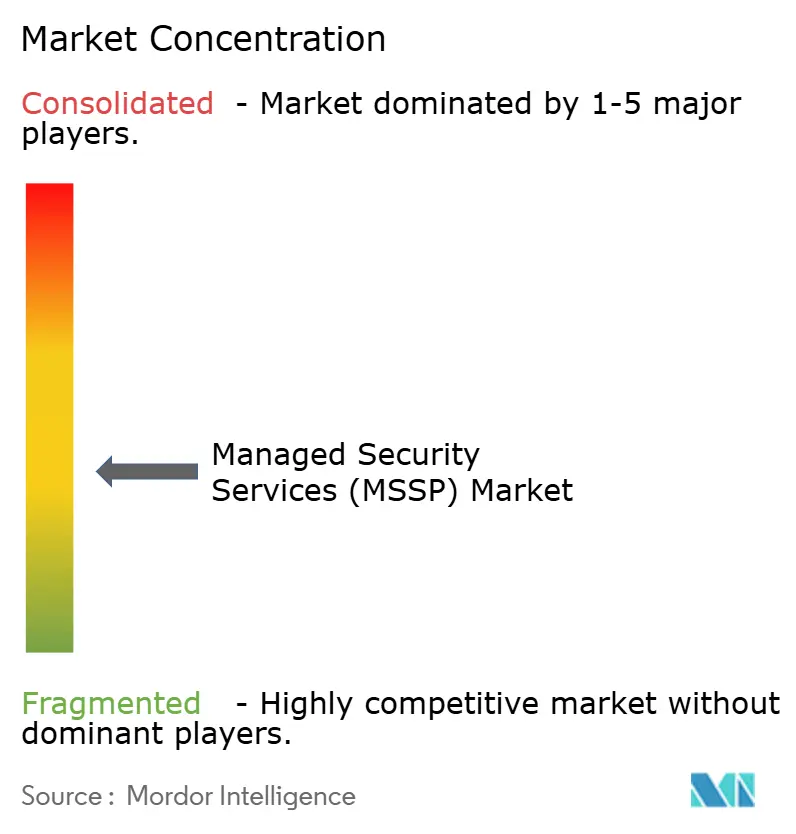

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Managed Security Services (MSSP) Market Analysis by Mordor Intelligence

The managed security services market size stands at USD 38.31 billion in 2025 and is forecast to reach USD 69.16 billion by 2030 at a 12.54% CAGR. Heightened regulatory pressure, notably the European Union’s DORA and NIS2 directives, drives enterprises to embed security controls at the design stage rather than bolting them on later. Organizations are moving from reactive defenses to AI-enabled, predictive threat detection that scales across hybrid environments. Accelerated cloud migration, widening multi-cloud attack surfaces and an intensifying cyber-talent shortage further enlarge outsourcing demand. Competition is intensifying as cloud hyperscalers integrate security analytics into their platforms, forcing traditional providers to differentiate through vertical expertise and unified security architectures. Consolidation continues, with 2024’s USD 859 million Sophos-Secureworks deal showing providers’ urgency to acquire advanced analytics capabilities.

Key Report Takeaways

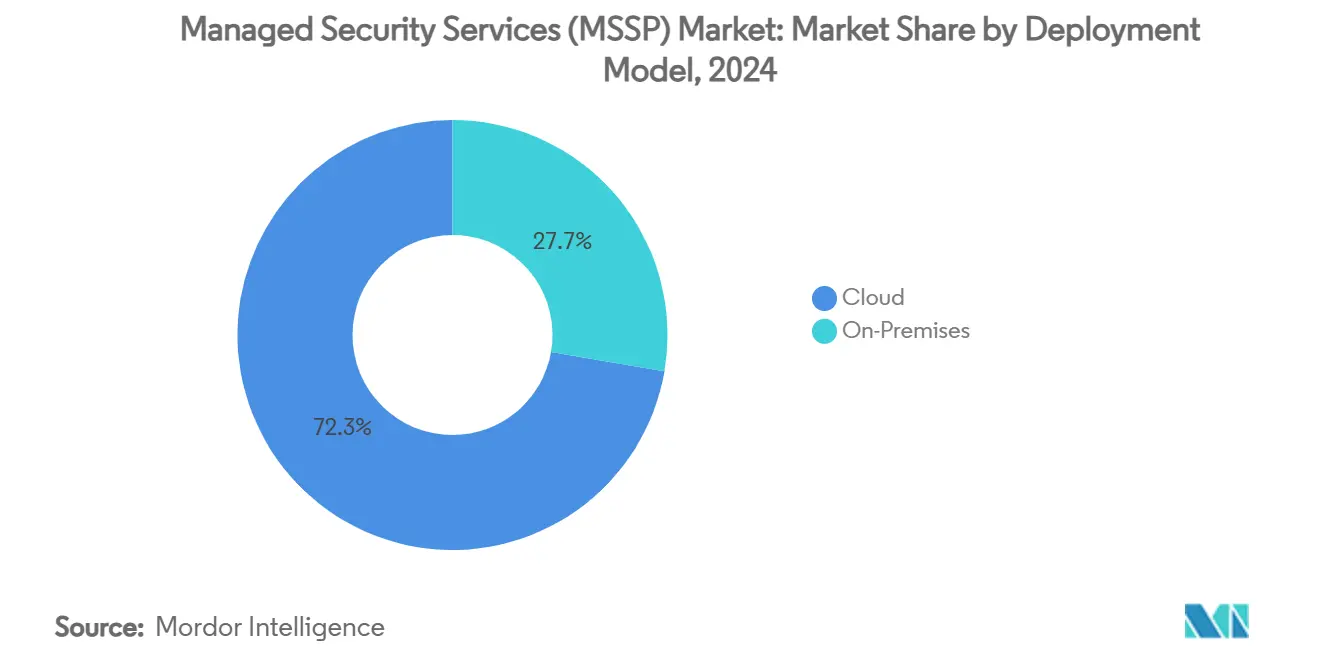

- By deployment model, cloud-based services led with 72.3% of managed security services market share in 2024; on-premises lags while cloud is growing at a 14.7% CAGR through 2030.

- By service type, Managed Detection and Response captured 27.3% of the managed security services market size in 2024 and is expanding at a 12.9% CAGR.

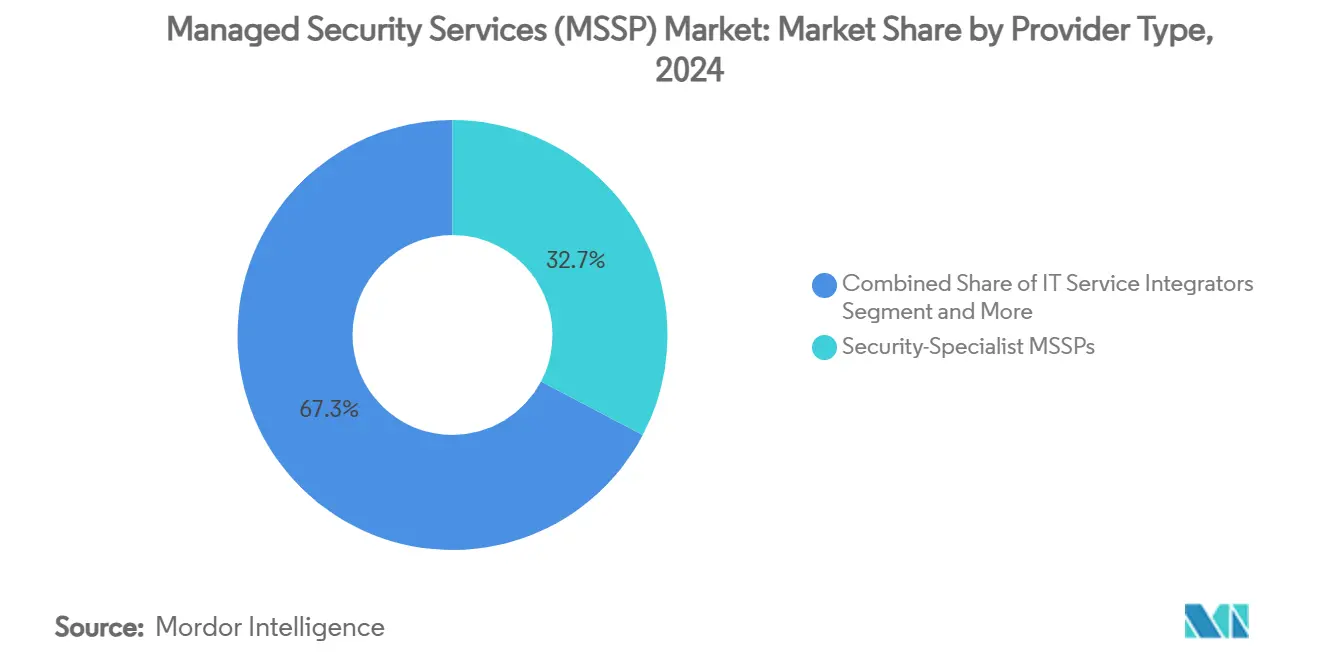

- By provider type, Security-Specialist MSSPs held 32.7% revenue share in 2024, whereas Cloud Hyperscaler MSSPs post the highest 14.2% CAGR to 2030.

- By end-user industry, BFSI led with 24.7% of the managed security services market share in 2024; healthcare is advancing fastest at a 13.4% CAGR.

- By geography, North America commanded 29.3% revenue share in 2024; Asia-Pacific is registering the highest 13.1% CAGR toward 2030.

Global Managed Security Services (MSSP) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-led SOC automation and XDR adoption surge | +2.1% | Global, with North America and EU leading | Medium term (2-4 years) |

| Escalating multi-cloud attack surface | +1.8% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Compliance-by-design mandates (DORA, NIS2, SEC) | +2.3% | EU primary, North America secondary | Short term (≤ 2 years) |

| Cost and talent crunch pushing co-managed MSS | +1.9% | Global, acute in Asia-Pacific and MEA | Medium term (2-4 years) |

| Rise of usage-based pricing and MDR bundling | +1.2% | North America and EU core, expanding globally | Long term (≥ 4 years) |

| Quantum-resistant encryption urgency | +0.9% | Global, government and BFSI priority | Long term (≥ 4 years) |

Source: Mordor Intelligence

AI-led SOC automation and XDR adoption surge

Organizations are embedding artificial intelligence into security operations centers to shorten detection and response cycles and limit analyst fatigue. Microsoft’s Security Copilot integrated with Defender XDR cuts mean time to respond by 40% and slashes false positives by 60%, showcasing how generative AI speeds triage and improves fidelity. Palo Alto Networks’ Cortex XSIAM already processes 1 trillion daily events to surface hidden attack paths, enabling MSSPs to deliver outcome-based SLAs that justify premium pricing.[1]Palo Alto Networks, “Cortex XSIAM: Autonomous SOC Platform,” paloaltonetworks.comThe approach also mitigates talent shortages, allowing 24/7 monitoring with smaller analyst teams. As AI-native competitors proliferate, traditional providers risk margin compression unless they embed autonomous investigation and response at scale. Over the medium term, successful MSSPs will fuse AI models with proprietary threat intelligence to anticipate attacks before initial compromise.

Escalating multi-cloud attack surface

Wide adoption of AWS, Azure and Google Cloud creates fragmented visibility, leaving security gaps that hackers exploit. CrowdStrike recorded a 75% year-over-year rise in cloud intrusions during 2024, driven by misconfigurations and over-privileged identities. Enterprises now juggle 3.2 security integrations per cloud, compounding alert noise. Google Cloud’s SecOps platform crunches 400 billion signals each day, illustrating the analytic horsepower needed to filter genuine threats.[2]Thales Group, “Thales and Google Cloud Partner on Global SOC Platform,” thalesgroup.com MSSPs able to ingest telemetry from multiple clouds into a single analytics fabric gain share by simplifying operations and cutting tool overheads. In the short term, demand for cloud-native threat monitoring outpaces supply of qualified experts, fueling double-digit growth across the managed security services market.

Compliance-by-design mandates (DORA, NIS2, SEC)

Regulators now expect continuous monitoring and real-time breach notification. From January 2025, DORA enforces strict ICT risk controls across EU financial entities, with penalties up to 2% of global turnover. SEC rules oblige US-listed firms to disclose material cyber incidents within 4 business days, elevating board-level focus on breach preparedness. NIS2 widens scope to 18 critical sectors, introducing fines of EUR 10 million or more for lapses. MSSPs that deliver automated compliance dashboards and regulatory-ready reports command higher margins while reducing enterprise audit overhead. Over the next two years, compliance-by-design thinking influences every new security architecture decision, intensifying subscription renewals across the managed security services market.

Cost and talent crunch pushing co-managed MSS

An 18-month vacancy for senior cyber roles and 23% annual inflation in tool licensing costs are unsustainable for many CISOs. Co-managed arrangements let enterprises keep strategic oversight while outsourcing deep-dive threat hunting, vulnerability scanning and incident response. N-able research shows clients on co-managed contracts improve mean-time-to-detect by 34% and cut security incidents by 42%. Mid-market organizations adopt the model fastest as it balances trust and budget. Across APAC and MEA, shortages of certified analysts are acute, so providers offering flexible staffing and shared governance frameworks are winning multi-year deals. Over the medium term the co-managed archetype becomes the entry point for customers hesitant to relinquish full control.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent trust deficit in data-sovereignty | -1.4% | EU and Asia-Pacific primary, regulatory driven | Medium term (2-4 years) |

| Tool sprawl and integration complexity | -1.1% | Global, acute in large enterprises | Short term (≤ 2 years) |

| Escalating liability exposure for MSSPs | -0.8% | North America and EU, insurance driven | Long term (≥ 4 years) |

| Short supply of OT-security specialists | -0.9% | Global, critical in manufacturing and energy | Medium term (2-4 years) |

Source: Mordor Intelligence

Persistent trust deficit in data-sovereignty

European clients balk at shipping telemetry to SOCs outside EU borders even when providers boast GDPR clauses. India, China and Brazil enforce localization statutes that fragment global delivery models, raising provider overheads. The 2025 Marks & Spencer breach, traced back to a third-party vendor, cost EUR 300 million in lost sales and amplified concerns over extended supply chains.[3]Sangfor Technologies, “Lessons from the 2025 Marks & Spencer Supply-Chain Breach,” sangfor.com To win contracts, MSSPs add domestic SOC footprints and guarantee residency for sensitive logs, but duplicating infrastructure erodes margins. Over the next three years, data-sovereignty constraints temper growth in heavily regulated verticals even as demand rises.

Tool sprawl and integration complexity

Enterprises run 45-60 disparate tools, creating alert fatigue and integration gaps that adversaries exploit. Kaspersky finds manufacturers deploy 12 separate OT-security products, complicating patch cycles and elevating risk. When MSSPs overlay their own tech stack, they face expensive API customization. Inefficiencies delay detection and raise service costs, narrowing the provider’s profitability window. Until unified platforms mature, large-scale deployments will experience onboarding friction that slows managed security services market expansion.

Segment Analysis

By Deployment Model: Cloud-Native Security Dominates

Cloud-based services accounted for 72.3% of the managed security services market in 2024 as enterprises re-platformed security controls alongside workloads. The segment is forecast to expand at a 14.7% CAGR through 2030, reflecting confidence in hyperscaler resilience and AI-infused analytics. Providers operate global PoPs that ingest logs at petabyte scale, then apply machine learning to spot lateral movement within minutes. Cost benefits compound adoption: CIOs report 45% lower total cost of ownership and 60% faster time-to-value compared with appliance-centric deployments. On-premises models persist in defense and highly classified environments where air-gap mandates override scalability concerns. Hybrid approaches emerge, with sensitive logs stored locally while non-classified telemetry streams to cloud SIEMs for aggregated analytics. The managed security services market size for cloud deployments is poised to widen its lead as 5G and edge compute push telemetry volumes higher. Meanwhile, providers redesign SLAs around latency and uptime guarantees to reassure regulated customers.

Second-generation cloud architectures emphasize API-level integration rather than lift-and-shift virtual appliances. Zscaler’s alliance with BT illustrates the model: BT funnels 400 billion daily sessions through Zscaler’s cloud to gain real-time risk scoring on every transaction. Such scale delivers threat intelligence inaccessible to siloed deployments, creating a feedback loop that continuously improves detection. Geopolitical tensions, however, force hyperscalers to build sovereign clouds, which may dilute centralization benefits. Nonetheless, with SaaS adoption in double digits, the managed security services market continues to pivot decisively toward cloud-first delivery.

By Service Type: MDR Leads Threat Detection Evolution

Managed Detection and Response held 27.3% of the managed security services market share in 2024, posting a 12.9% CAGR as customers demand active containment rather than ticket-only monitoring. MDR fuses endpoint telemetry, network flow data and identity context to surface anomalous behavior. Providers couple 24/7 analyst eyes with automated response playbooks, isolating patient-zero hosts in seconds. Traditional firewall management faces commoditization, but remains necessary for compliance-driven perimeter controls. Identity-centric zero-trust services are rising, particularly among SaaS-heavy mid-size enterprises.

AI-enabled MDR platforms such as Red Canary’s Managed XSIAM harness log-correlation engines to cut dwell time and shrink breach impact. Increased pairing of MDR with vulnerability management supports continuous remediation loops. DDoS mitigation stays relevant for uptime assurance, while managed IAM services close privilege-escalation gaps. Overall, layered MDR bundles position providers as strategic partners, underpinning sticky three- to five-year contracts that swell the managed security services market size for outcome-focused offerings.

By Provider Type: Specialists Face Hyperscaler Challenge

Security-specialist MSSPs captured 32.7% revenue in 2024 due to domain depth and curated threat feeds. Yet hyperscaler-aligned MSSPs are expanding at 14.2% CAGR, fueled by native telemetry access and AI tooling embedded in cloud consoles. Enterprises migrating workloads to public clouds view single-pane-of-glass security appealing, eroding loyalty to standalone providers. IT integrators and telecom carriers pivot by bundling secure connectivity with SOC services, chasing margin in value-added analytics rather than bandwidth.

AT&T Dynamic Defense merges network edge data with Palo Alto’s threat engine to differentiate on end-to-end visibility. Consulting-led cyber practices focus on governance, risk and compliance where advisory margins remain robust. Ongoing M&A USD 45.7 billion in 2024 accelerates convergence, prompting mid-tier players to form alliances or risk irrelevance. As hyperscalers emphasize turnkey security, specialists double down on vertical niches like OT or crypto-agility, sustaining diversity within the managed security services market.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Healthcare Accelerates Past BFSI

BFSI retained top spot with 24.7% share of the managed security services market in 2024, but growth is flattening relative to earlier years. Stringent DORA and SEC rules keep spending elevated, yet banks have matured SOC practices and negotiate aggressively on price. Healthcare, posting a 13.4% CAGR, now drives incremental expansion. Digitization of clinical workflows, proliferation of IoT medical devices and tighter privacy statutes push hospitals toward outsourced monitoring.

BestSelf Behavioral Health’s adoption of 24/7 managed SOC exemplifies how providers mitigate patient data exposure while tapping MSSP regulatory playbooks. Government and defense entities value air-gapped SOCs, while manufacturing grapples with OT asset visibility gaps. Retail and eCommerce depend on card-holder data security and bot-defense, but seasonality shapes procurement cycles. Energy utilities prioritize NERC CIP and IEC 62443 adherence, demanding engineers conversant with SCADA protocols. These vertical nuances encourage MSSPs to spin industry-specific service lines, deepening segmentation across the managed security services market.

Geography Analysis

North America held 29.3% of global revenue in 2024, buoyed by stringent SEC disclosure rules and ready access to venture funding that fuels security innovation. US firms lead adoption of AI-driven SOCs and quantum-resistant pilots, whereas Canadian utilities focus on critical-infrastructure hardening aligned with C-SCRM guidance. Mexico’s automotive corridor embraces co-managed SOCs to offset talent deficits. Despite saturation at large enterprises, mid-market penetration remains underscored by ransomware’s financial impact, sustaining double-digit spend.

Asia-Pacific is growing fastest at 13.1% CAGR through 2030. Japan’s manufacturers fortify OT assets after multiple supply-chain breaches; China emphasizes domestically developed SOC platforms under data-localization mandates; India’s small and mid-size firms outsource log monitoring to bridge skills shortfalls. ASEAN banks face digital-payments fraud surges, prodding regulators to raise breach-reporting fines that boost managed security services market demand. South Korea pioneers 5G-edge protection frameworks, positioning local MSSPs as exporters of MEC-centric threat analytics.

Europe advances steadily due to DORA and NIS2. Germany invests in industrial-control defenses, the UK emphasizes financial-sector resilience post-Brexit, and France nurtures sovereign-cloud SOCs. Mediterranean SMEs turn to MDR subscriptions to meet insurance prerequisites. Data-residency stipulations favor regional SOC buildouts, compelling global providers to partner with domestic data-center operators. Collectively, regulatory harmonization and funding initiatives anchor a compliance-driven managed security services market across the continent.

Competitive Landscape

The market remains moderately fragmented as no single provider exceeds one-third of revenue. Security specialists, hyperscaler affiliates, telecom carriers and consulting practices jostle for wallet share. AI-first entrants tout faster MTTR, flooding prospects with benchmark statistics; incumbents respond by integrating XDR stacks and automating playbooks. Strategic alliances surge: Verizon pairs with Accenture for identity services, Kyndryl teams with Microsoft for data-security-posture management. Platform convergence underpins USD 45.7 billion of 2024 M&A, epitomized by Sophos acquiring Secureworks to couple endpoint and network telemetry.

White-space opportunities emerge around OT visibility, quantum-safe crypto migration and usage-based billing. Providers capturing unique telemetry—mobile networks, satellite links or industrial sensors—differentiate through proprietary threat intelligence. Still, liability exposure and insurance constraints deter smaller entrants. Over 2025-2028, expect more roll-ups as mid-cap MSSPs seek capital to fund sovereign SOC footprints required by local regulators. Competition, however, also broadens: cloud hyperscalers embed zero-trust and SIEM in subscription bundles, challenging independent SOC providers to justify incremental value.

Managed Security Services (MSSP) Industry Leaders

-

AT&T Inc.

-

Secureworks Corp.

-

Broadcom Inc.

-

Trustwave Holdings, Inc. (the Chertoff Group)

-

Fortra, Llc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: T-Mobile and Palo Alto Networks launched T-Mobile SASE with Palo Alto Networks, combining nationwide 5G Advanced coverage and Prisma SASE to deliver unified connectivity and security.

- April 2025: Kyndryl and Microsoft unveiled Kyndryl Consult Data Security Posture Management, using Azure-native AI to strengthen hybrid-cloud data protection.

- April 2025: AT&T and Palo Alto Networks introduced AT&T Dynamic Defense, blending network telemetry with AI-driven prevention for real-time risk response.

- March 2025: Verizon Business and Accenture formed a partnership to enhance identity, managed XDR and cyber-risk advisory services.

- January 2025: Cognizant partnered with CrowdStrike to pair the Falcon platform with Cognizant’s Neuro Cybersecurity framework for improved cloud breach defense.

Global Managed Security Services (MSSP) Market Report Scope

The managed security service market is defined by the revenues generated from diverse solutions used across various industries worldwide. The analysis draws from both primary and secondary research, capturing market insights. It delves into the key drivers and restraints shaping the market's growth.

The managed security services market is segmented by deployment type (on-premise and cloud), by solution type (intrusion detection and prevention, threat prevention, distributed denial of services, firewall management, end-point security, and risk assessment), by managed security service provider (IT service providers, managed security specialist, and telecom service provider), by end-user industry (BFSI, government and defense, retail, manufacturing, healthcare and life sciences, IT and telecom, and other end-user verticals), and by geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| By Deployment Model | On-Premise | |||

| Cloud | ||||

| By Service Type | Managed Detection and Response (MDR) | |||

| Firewall and UTM Management | ||||

| Intrusion Detection/Prevention | ||||

| Managed IAM and Zero-Trust | ||||

| DDoS and Threat Prevention | ||||

| Vulnerability and Patch Management | ||||

| Others | ||||

| By Provider Type | IT Service Integrators | |||

| Security-Specialist MSSPs | ||||

| Telecom-Led MSSPs | ||||

| Cloud Hyperscaler MSSPs | ||||

| Consulting-Led Cyber Practices | ||||

| By End-user Industry | BFSI | |||

| Government and Defense | ||||

| Healthcare and Life Sciences | ||||

| Manufacturing and Industrial | ||||

| Retail and eCommerce | ||||

| IT and Telecom | ||||

| Energy and Utilities | ||||

| Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Southeast Asia | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| On-Premise |

| Cloud |

| Managed Detection and Response (MDR) |

| Firewall and UTM Management |

| Intrusion Detection/Prevention |

| Managed IAM and Zero-Trust |

| DDoS and Threat Prevention |

| Vulnerability and Patch Management |

| Others |

| IT Service Integrators |

| Security-Specialist MSSPs |

| Telecom-Led MSSPs |

| Cloud Hyperscaler MSSPs |

| Consulting-Led Cyber Practices |

| BFSI |

| Government and Defense |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Retail and eCommerce |

| IT and Telecom |

| Energy and Utilities |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the global managed security services market size in 2025?

The market is valued at USD 38.31 billion in 2025.

Which deployment model currently commands the largest share of the managed security services market?

Cloud-based delivery leads with a 72.3% share as of 2024.

Which geographic region is expected to grow fastest in managed security services?

Asia-Pacific is forecast to grow at a 13.1% CAGR through 2030.

What new regulation is accelerating managed security services adoption in Europe?

The Digital Operational Resilience Act (DORA) requires continuous ICT risk management for financial entities starting January 2025.

Page last updated on: July 6, 2025